They Will Tell You the Well Is Dry [Part 2]

They will tell you the well is dry while they are swimming in it

There is a story the industry tells itself, and it tells it constantly, with great conviction. The story, goes like this: the money is gone. Audiences are not going to theaters anymore. The economics of film simply do not work the way they used to. It is a hard time for everyone. Everyone, that is, except the people telling the story.

What the numbers say and what the industry says about the numbers are not always the same conversation. In 2024, Warner Bros. Discovery CEO David Zaslav took home a compensation package worth $51.9 million, up from $49.7 million the year before. The median WBD employee had annual total compensation of $130,316, putting the pay ratio of the CEO to that median employee at 398 to 1. At Disney, Bob Iger earned $41.1 million in 2024, a 30 percent increase over the year before, in a year that also saw mass layoffs ultimately affecting more than 8,000 workers, described publicly as necessary budgetary measures. At Netflix, co-CEOs Ted Sarandos and Greg Peters each took home over $53 million in total compensation in 2025. The CFO, Spencer Neumann, made $22.9 million in total compensation for the 2024 fiscal year. These are not the numbers of an industry that cannot afford to pay its people. These are the numbers of an industry that has decided, with great precision, who gets paid and who does not.

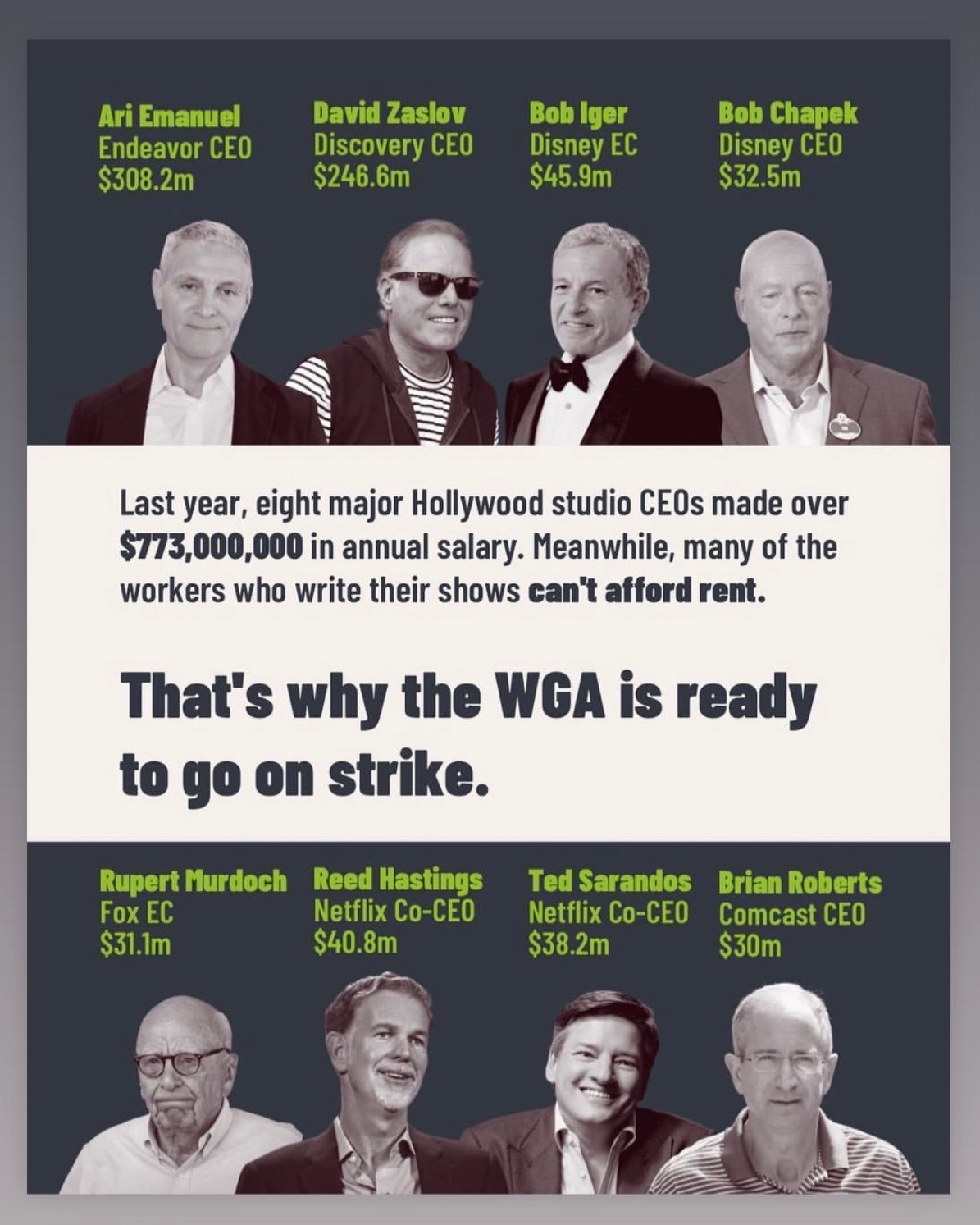

Guild members were circulating this image of CEO 2021 pay.

This distinction was never more visible than during the WGA strike of 2023, when writers spent 148 days on picket lines fighting for wages, staffing minimums, and protections against the AI tools that studios were openly discussing as cost-cutting instruments. While that was happening, the WGA shared an infographic outlining the $773 million in combined salary that eight major Hollywood studio CEOs made in 2021 alone, noting that many of the workers who write their shows cannot afford rent. Bob Iger, during the strike, told CNBC that the writers' and actors' demands were "not realistic," a characterization that landed with particular force given what his own compensation package looked like at the time. (Again, Bob Iger earned $41.1 million in 2024, a 30 percent increase over the year before.)

The Empty Theater That Is Not Actually Empty

The second myth runs alongside the first and supports it: nobody is going to the movies anymore. The data does not support this. What it actually shows is something more specific and more damning for the people making the argument. When audiences are given films worth seeing, they show up. Barbie and Oppenheimer together generated one of the most remarkable theatrical events in recent memory. Sinners, Ryan Coogler's original musical horror film set in the Jim Crow South, grossed $370 million worldwide and became the highest-grossing original film of the last fifteen years. Weapons, Zach Cregger's supernatural mystery made for $38 million, grossed $270 million against that budget, a return that no franchise arithmetic was required to produce. And Obsession, Curry Barker's debut feature made for $1 million, was acquired out of Toronto for $15 million and opened to strong reviews and an audience that came out opening weekend. The audience was never the problem.

The festival data makes this even harder to ignore. Festivals have begun to feel less essential to the industry even as they become more meaningful to audiences. That is not a minor distinction. It describes an audience that is actively seeking out smaller, more personal, more artistically driven work and finding it at festivals because the traditional distribution system has stopped making it available to them anywhere else. Eventive's data, pulled from ten million tickets across more than 2,400 festivals, shows festival revenue up 36 percent compared to pre-pandemic levels, with average ticket sales per event back to where they were before 2020. Meanwhile, a Harvard study led by former Sundance Institute CEO Keri Putnam found that approximately 6.6 million people attended U.S. film festivals in 2023, but the estimated fan base is closer to 20 million, representing a massive gap between the people showing up and those who could be reached. More striking still, the study identified an estimated 40 million Americans who are interested in independent film but are not currently being captured by traditional distribution.

The audience exists. It has not been lost so much as underleveraged, by a system that confused a supply and marketing problem for a demand crisis. The studios chose not to make certain films. They chose to minimally market some of the ones they did make. The resulting underperformance became evidence, in their telling, that the audience had disappeared. Forty million people would suggest otherwise.

The marketing argument deserves its own paragraph because it is where the abdication is most visible. The studios that built the art of the theatrical campaign, that understood how to make a film feel like a cultural event worth leaving the house for, have largely dismantled those capabilities. In a world where audiences are being pulled in more directions than ever before, the response has been to concentrate resources on tentpole films and reduce investment everywhere else. The trailers that play before films have grown so long that the theatrical experience itself becomes a test of endurance before the film you paid to see has even begun. The exhibitors, for their part, have done little to reimagine an experience that might justify the effort of showing up. Nobody is going to the movies anymore, the industry says, while cutting marketing budgets, releasing films without campaigns, and wondering why nobody came.

The Terms of Entry

The well is not dry. The money exists. The question is who it is flowing toward and who is being told, with great regret and considerable corporate language, that there simply is not enough to go around.

When filmmakers mention releasing their own films directly, people inside the system tend to react as though something delusional has been said. The assumption embedded in that reaction is that distribution is something that happens to you, something granted by an institution with the resources and relationships to do it properly. The idea that the people who raised the money, developed the project, produced the film, and spent careers learning how to market things might also be capable of getting it to an audience is treated as charming at best and naive at worst.

But consider the actual structure of what we are describing. We bring a project to a market that has largely moved from taking developmental bets to ratifying proven ones. We then hand distribution to institutions that are, at the same moment, making the case that the economics do not allow for more generous terms with the people doing the work. If the system is no longer investing in the development of art, only in the confirmation of it, the question worth sitting with is a simple one: what exactly are we still asking permission for?

The people making those arguments are not wrong that the economics are under pressure. They are simply consistent about who bears it. The writers on the picket line in 2023 bore it. The indie producers developing projects on their own dime bear it. The directors who run the festival gauntlet bear it. The CEOs, by any available measure, do not.

The System is Not Broke

It is redistributing. And it has been doing so for long enough, and visibly enough, that the argument for building something outside it becomes not just idealistic but logical. We are not doing it out of bitterness. Bitterness is a waste of a resource that could be spent making things.

What we are doing is something more straightforward: reading the room. Understanding the game being played, and making a considered decision about how we want to participate in it. That is not rebellion. That is realism about what the market will bear, paired with the optimism to believe you can meet it.

We launched VOKSEE in 2015 as a production company built around a specific belief: that the industry was trending in a direction that would require a different kind of infrastructure to sustain the work we wanted to make. Eleven years later, that assessment has held. In that time we have navigated a global pandemic that shuttered production across the industry, a writers strike that laid bare every tension this series has been describing, and the devastating Los Angeles fires that took from this community in ways that went far beyond the professional. None of it was part of the plan. All of it clarified what the plan needed to be.

The studio system is not the enemy. It is important to say that plainly, because nothing in this series is meant to suggest otherwise. The studio system, at its best, has been one of the great champions of storytelling in the history of human culture. It built the infrastructure that made cinema a global language. It developed voices, took risks, and at its most meaningful, created the conditions for artists to make work that outlasted any balance sheet. I believe that is still true in pockets, still possible in corners of the system where the right people are making the right calls. For those with internal influence, please use it. The programs that develop new voices, that take early bets on emerging filmmakers, are worth fighting for from the inside. We are doing it with an indie budget and a long term belief in the work. The resources exist inside the system to do it at a scale we can only dream about.

The past two parts of this series have been about one thing: knowing where you stand. Knowing what the terrain looks like before you start walking across it. The threats are real, the data is unambiguous, and the imbalances are significant. But none of that is the conclusion. It is the context. And context, understood clearly, is where opportunity begins.

The third and final part of this series is about exactly that. The greener pastures.

(Part 2 of 3. Part Three: Show Up to the Audition Like You Already Have the Part - publishes next week. Subscribe to the newsletter for a reminder, or go ahead and block the time now.)

* While this series has been written from the perspective of film, the dynamics at play, the systems, the economics, the relationship between artist and institution, exist across every creative industry.

** It is worth noting, and we will get into this in the final part of this series, that budget discipline is one of the industry's least discussed and most consequential problems. It touches every area of the business: development, production, marketing, publicity, operations. The issue is not always that movies cost too much. It is that too many movies are made at the wrong cost for the story they are telling and the audience they are trying to reach. Sadly, some of this is industry strategy, structural and deliberate. But for independent filmmakers navigating this landscape, understanding the economics is not optional. Being in service of the craft, your crew, your investors, and your partners requires it. Fiscal responsibility is a core belief of mine, and one I would argue is inseparable from the creative process itself. It is an expression of respect for everyone who has bet on you to get it right.